Existing Charity, starting using the system from the start of a new financial reporting period

Correct opening balances are the key to bookkeeping activities. If you do not enter them accurately your accounts will be wrong (although adjustments can be made subsequently, it is recommended that the opening balances should be correct to begin with). Entering opening balances, although not as straightforward as most other processes, can be achieved by following the instructions accurately. Ensure that you have all the relevant information to hand for each stage of the procedure before starting.

The Opening Balance Date

The opening balances that you input must represent the financial position of your organisation on the day you start entering live transactions. This usually means entering a trial balance dated the day before the first day of the new accounting period.

The system derives the date by taking the the day just prior to the Liberty Accounts Start Date that is set on the Organisation Profile.

Control - Organisation Profile - Accounting Options Tav

Information needed and appropriate dates

| as at prior period end date | as at opening balance date |

|---|---|

| - balance for each fund | |

| - income/expense balance by account by fund (for comparatives) | - balance for each asset account |

| - balance for each liability account (except funds) |

This guide addresses the following topics: -

- What are Opening Balances?

- What is a trial balance?

- Opening Balances Procedure in Summary

- The Opening Balances Process

- Define Funds

- Define Activities(if required)

- Define additional bank and credit card account (if required)

- Opening Balances for Bank Accounts

- Opening Balances for Customers and/or Suppliers(if required)

- Opening Balances of Tangible Fixed Assets(if required)

- Opening Balances for Other Assets(if required)

- Opening Balances for Other Liabilities (if required)

- Prior Year Comparatives for Income and Expenditure

- Setting up a donor ledger (if required)

- Completing the Opening Balances Process

What are Opening Balances?

Opening balances represent a snap shot of the financial state of your organisation at the date of starting with the system. The following types of data are usually needed: -

- Details of Funds and Fund balances

- Bank account balances.

- Customer transactions that have not been completed such as invoices that have been issued but not yet paid by the client/

- Supplier transactions that have not been completed, bills for goods or services received but not yet paid, tax and VAT payments still to be made to the authorities.

- Other information such as the values of assets, capital, stock or hire purchase agreements.

What is a trial balance?

A trial balance is a list of all the accounts (chart of accounts), at a given date, together with the value shown either as a debit or credit balance. In a double entry bookkeeping system, if correct, the sum of all debit balances equals the sum of all credit balances.

| Account | Debit | Credit |

|---|---|---|

| Capital | 3000 | |

| Borrowing | 5000 | |

| Rent | 200 | |

| Equipment | 1500 | |

| Wages | 100 | |

| Materials | 590 | |

| Sales | 450 | |

| Bank Account | 6150 | |

| TOTAL | 8450 | 8450 |

For a bank account in which you may have money, the statement will show this as a credit balance; you are in credit with the bank. However in a trial balance because the money in the bank is an asset, something you own, it is shown as a debit. An overdraft or bank loan would be shown as a credit. All assets are shown as debits and all liabilities are shown as credits.

Return to the list of topics in this user guideOperating Balances Procedure in Summary

It is strongly recommend that advice be sought from your accountant or advisor if you are unsure about setting up your opening balances.

- Set up details of the Charities funds and the opening balances

- Set up details of any Activities

- Set any bank and credit card accounts for which opening balances are required and any additional accounts required

- Set up and enter balances for the organisations bank accounts

- If you have customers and suppliers any outstanding balances need to be entered first

- If you are using fixed assets in your business and recording them as part of your business, items such as equipment, computers, vehicles etc. We would advise details of these items entered in the asset ledger

- Enter opening balances for the rest of your accounts (chart of accounts)

- This will be split up into four smaller pieces of input: -

- Assets

- Funds opening balances and if they exist other liabilities

- Income (Prior Year figures as comparatives)

- Expenses (Prior Year figures as comparatives)

- Print your trial balance and verify all figures. Suspense account should be zero

The Opening Balance Process

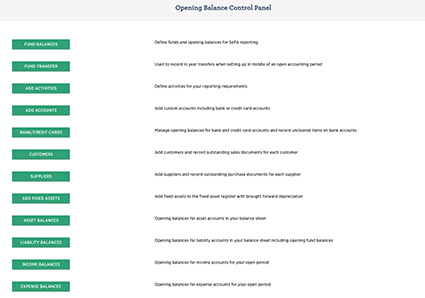

The Opening balance processes are grouped together under the Control menu in an Opening Balance Control Panel.

Control - Opening Balances

The panel has input processes for each major element of the opening balance process. Progress notes indicate any balance on the suspense account; it should be zero when all opening balances have been input.

Return to the list of topics in this user guideDefine Funds

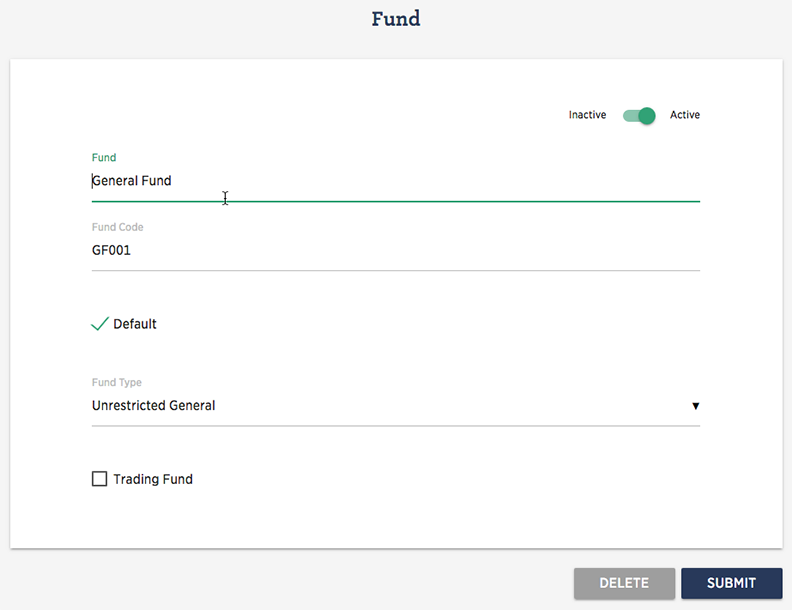

At least one fund must be defined, but as many funds as are necessary may be set up and reported on. Click on the red + symbol to enter a new Fund, the details are entered in the Fund Maintenance screen.

As each fund is set up, in the chart of accounts a sub-account of Retained Funds is created with the same name as the fund, and displaying the fund balance.

Control - Opening Balances - Fund Balances

- Inactive/Active toggle (only displays once a fund has been added)

- Allows fund to be de-activated, if visible leave toggled to active

- Fund

- Enter name of the Fund

- Fund Type

- Select an appropriate fund type from the drop-down selection of:

- Endowment Capital

- Endowment Expendable

- Restricted

- Unrestricted Designated

- Unrestricted General

- Default

- If ticked, becomes the default fund selection where there are multiple funds

- Trading Fund

- Tick to indicate the fund is a trading fund.

Click SUBMIT when complete. Repeat for as many funds are required.

An opening balance for each fund displayed must be entered to ensure that the SoFA is accurate. The opening balances that you input must represent the financial position of your organisation on the day you start entering live transactions.

The display is impacted by the SoFA reporting selection made when organisation was set up. (The user can inspect this by navigating to the Organisation Profile)

Control - Organisation Profile - Accounting Options tab

If the Income & Expenditure basis is chosen only I&E Opening Balances are entered.

If Receipts & Payments is selected then both I&E and R&P Opening balances are entered and a R&P balance start date.

Enter the date to which the R&P opening balance amounts are related. This date may or may not be the same date as the Organisation overall opening balance date.

Return to the list of topics in this user guideDefine Activities

Activities may be used to analyse transactions to charitable activities such as projects, initiatives or other analysis. This is in addition to any specific accounts set up within the chart of accounts for recording to activities of the charity. The details are entered in the Activity Maintenance screen in a similar manner to funds above.

Control - Opening Balances - Add Activities

Ignore if Activity analysis is not required.

Return to the list of topics in this user guideOpening Balances for Bank Accounts

At least one bank account is required for the system to operate. A bank account was probably created at the time of setting up the entity, but if not, then an account needs to be set up at this stage.

See Opening Balances for Bank Accounts for more detailed guidance.

Return to the list of topics in this user guideOpening Balances for Customers and Suppliers

If the opening trial balance includes customer and/or supplier opening balances (Unpaid Invoices or Bills) then these may be entered using a routine as described in the link Opening Balances for customers and/or suppliers.

Ignore if there are no opening balances for customers or suppliers.

Return to the list of topics in this user guideOpening Balances of Tangible Fixed Assets

If the business is using tangible fixed assets (Machinery, Computers, Vehicles etc.) then the trial balance will include amounts for the value of these assets. The value of these assets will have to be entered as opening balances for the original cost or valuation of the assets and the cumulative depreciation.

See Opening Balances of Tangible Fixed Assets for more detailed guidance.

Return to the list of topics in this user guideOpening Balances for Other Assets

The trial balance may well include items such as Stocks, Investments and other debtors, these are input via using a routine as described in the link Opening Balances of other assets.

Return to the list of topics in this user guideOpening Balances for Liabilities

The trial balance may well include items such as borrowings, payroll deduction liabilities these are input via using a routine as described in the link Opening Balances for Liabilities.

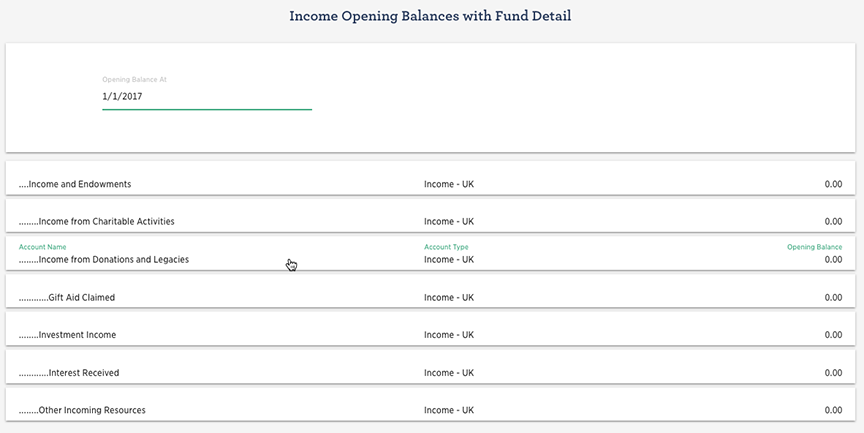

Return to the list of topics in this user guidePrior Year Comparatives for Income and Expenditure

There are screens provided for this accessed as follows:

Control - Opening Balance - Income Balances

Control - Opening Balance - Expense Balance

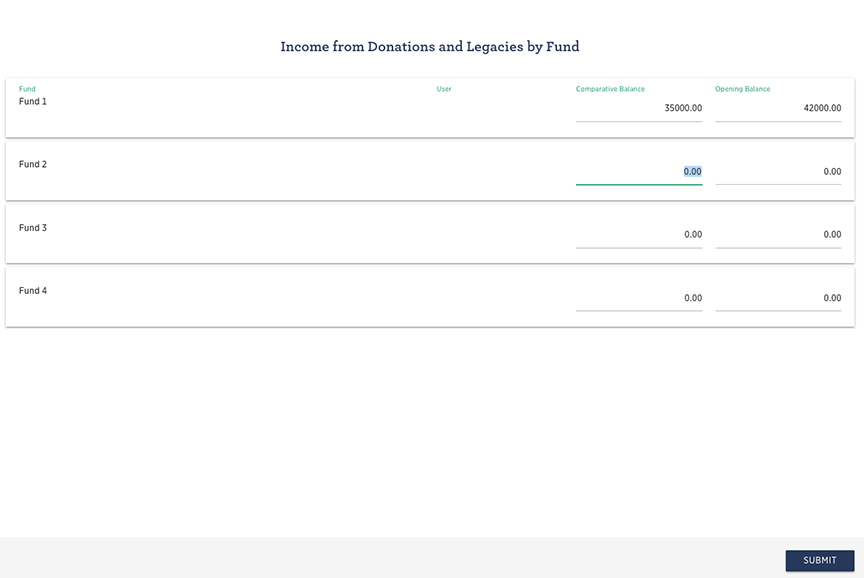

Click on each account for which an opening amount is to be entered

A dialogue screen is presented to allow the user to enter

- Balance by fund as at the prior period end date. This is used for comparative figures on the SOFA

Do not enter anything in the opening balance column as the system is starting to be used from the beginning of the new financial period.

Complete for all income and expense accounts

Return to the list of topics in this user guideSetting up a donor ledger

If the organisation is receiving donations and claiming gift aid on some or all of those donations it would be helpful to set up the donation ledger in preparation for recording future donations and preparing claims.

See Setting up Donor ledger and Gift Aid for details.

Return to the list of topics in this user guideCompleting the Opening Balances Process

Print out the Trial Balance Report. This is accessed via the Reports menu.

Reports - Trial Balance

Select the Opening balance date.

If all has gone well the balance on the Suspense Account will be zero. If not print out the trial balance report and carefully review and check each figure against your original input data or trial balance.

You will need to check that:

- Opening balances for all your nominal accounts from your full trial balance have been entered

- An opening balance has not been entered twice

- Balances have not been entered as debits when they should be credits and vice versa

Go back and make any necessary amendments and reprint trial balance report. Confirm that it is now correct.

Congratulations you have now completed your opening balance procedure.

Return to the list of topics in this user guide